Embedded Finance: The Emergence of Pay-by-Bank Solutions

The Emergence of Pay-by-Bank Solutions

Pay-by-bank solutions, also known as bank-to-bank payments or open banking payments, leverage the infrastructure of traditional banking systems to facilitate transactions directly from a consumer's bank account to a merchant's account. Unlike conventional payment methods that rely on card networks or third-party processors, pay-by-bank solutions completely cut out intermediaries, resulting in faster settlement times and lower transaction costs.

Understanding Embedded Finance

Embedded finance refers to the seamless integration of financial services into non-financial platforms, enabling financial products like payments, lending, and insurance to be offered directly within apps or websites that aren't traditionally financial. This integration makes transactions smoother and more embedded into our daily lives, such as buying goods through a marketplace, or when booking a flight, or even securing a loan while shopping online. Embedded finance is built upon APIs (Application Programming Interfaces), partnerships between fintechs and traditional financial institutions, and robust API management measures.

Mobile payments have surged, with solutions like Apple Pay and Google Wallet leading the way by providing convenient payment options and streamlining the checkout process. However, pay-by-bank solutions can bypass these intermediaries, offering just as much convenience at a better price by enabling direct payments from bank accounts and reducing transaction fees.

Enabling Pay-by-Bank Solutions

Pay-by-bank solutions enable consumers to make payments directly from their bank accounts by embedding payment services into legacy banking systems and bypassing traditional intermediaries, like card networks. These solutions use secure APIs to connect merchants with consumers' banks, facilitating real-time payments. Key components include authentication mechanisms, instant transaction processing, and integration with existing banking infrastructure.

How It Works

- Initiation: The payment process begins when a consumer selects the pay-by-bank option at checkout on an e-commerce platform or mobile app.

- Authentication: The consumer is redirected to their online banking portal, where they securely authenticate the transaction using their banking credentials.

- Authorization: Once authenticated, the payment is authorized directly from the consumer's bank account to the merchant's account in real time.

- Confirmation: Upon successful completion, both the consumer and the merchant receive instant confirmation of the transaction.

Advantages of Pay-by-Bank Solutions

Enhanced Security

Pay-by-bank solutions prioritize security by leveraging established banking protocols and authentication mechanisms. By authenticating transactions directly through the consumer's bank, they significantly reduce the risk of fraud and unauthorized access. This method eliminates the need to expose card details, which are often targeted by cybercriminals. Secure APIs ensure that sensitive information, such as login credentials, is protected during transactions, making it much harder for cybercriminals to intercept and misuse the data.

Cost-Effectiveness

Traditional payment methods often incur fees associated with card processing or intermediary services. By bypassing card networks, pay-by-bank solutions significantly reduce transaction fees. This is particularly beneficial for businesses that process a high volume of transactions, lowering operational costs. Pay-by-bank solutions potentially offer savings that can be passed on to consumers.

Faster Transactions

Real-time processing is a key advantage of pay-by-bank solutions. Unlike traditional methods that can take several days to settle, pay-by-bank transactions are completed instantly, improving cash flow for businesses. By eliminating the need for manual entry of card details or account information, these solutions streamline the checkout process, reducing friction and cart abandonment rates. Consumers can complete transactions with just a few clicks, leading to higher conversion rates.

The Role of Open Banking in Embedded Payments

Open banking is central to the success of pay-by-bank solutions. It allows third-party developers to access financial data and services through APIs (Application Programming Interfaces). This access enables innovative payment processors to create user-friendly payment solutions that leverage the robust banking infrastructure. By removing intermediaries, both banks and customers benefit from greater control over their data, allowing them to be selective about who they share it with. This combination of stability from traditional banking and the agility of specialized fintech offerings results in highly efficient and convenient payment options for consumers.

Connecting the Fintech Ecosystem

Ecosystem integration is crucial for the success of pay-by-bank solutions and requires cooperation between traditional banks and fintechs, ensuring financial services are embedded seamlessly into various applications.

Benefits of Successful Integration

- Enhanced User Experience: Direct payments from bank accounts through platforms like e-commerce or mobile apps streamline the checkout process.

- Cost and Time Efficiency: Reduces transaction times and costs by skipping intermediaries, making the service more cost-efficient for users.

- Innovation and Stability: Combines fintech's innovative methods with the reliability of traditional banks and credit unions.

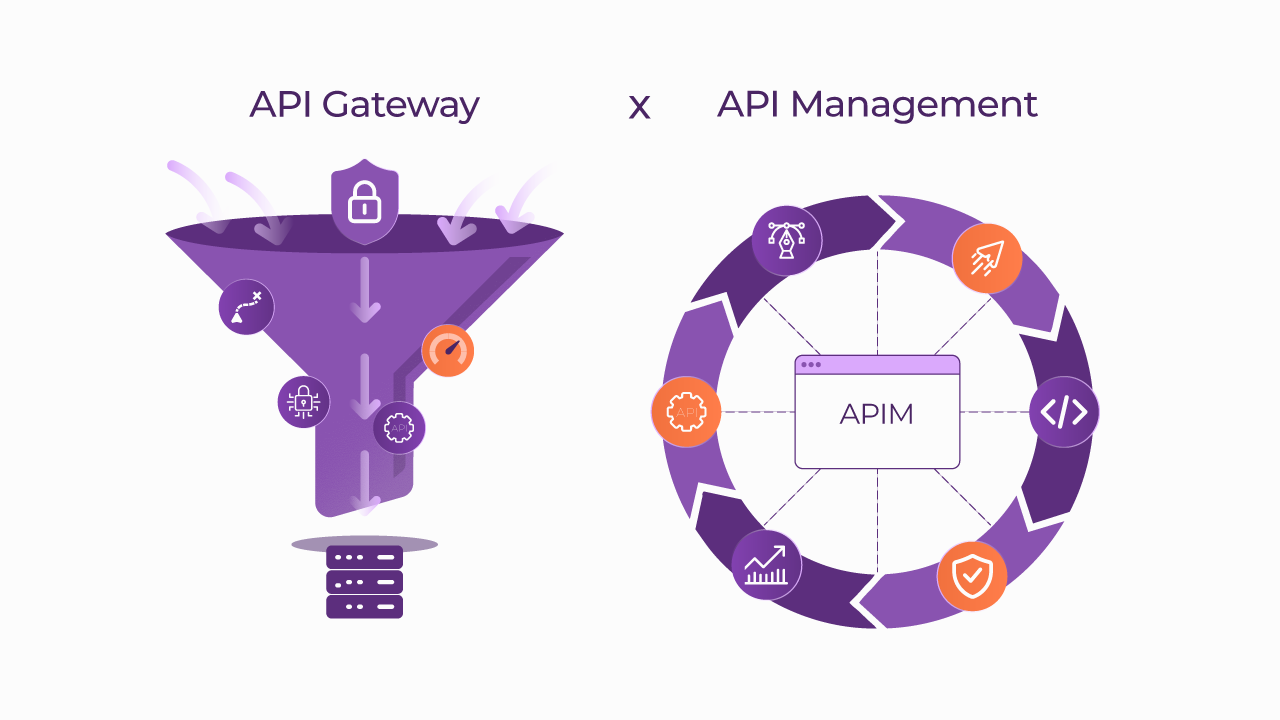

The Role of API Management

API management is a critical component in ecosystem integration. It facilitates connections between different systems and plays a vital role in analyzing and troubleshooting business revenue streams in real time. Proper API management ensures that data is handled securely and that user consent is well governed, helping maintain consumer trust and compliance with regulatory standards, while providing real-time observability into business processes.

Key Aspects of API Management

- System Integration: Ensures realiable communication between banking systems and fintech applications.

- Business Observability: Analyzes transaction data in real-time, providing insights into consumer behavior and revenue streams.

- Data Security: Implements encryption and access controls to protect sensitive information.

- User Consent Management: Ensures users are aware of how their data is used and have given explicit permission, building trust and complying with regulations like GDPR and CCPA.

By employing a platform approach and working together, banks can leverage fintech's agility and innovative products, while fintechs benefit from the stability and trust established by traditional financial institutions. This collaboration results in payment solutions that are not only efficient but also secure and reliable, offering a superior user experience that generates increased loyalty and revenues.

For businesses aiming to deliver modern solutions through embedded finance and open banking, discover more here:

https://www.sensedia.com/industry/financial

Begin your API journey with Sensedia

Hop on our kombi bus and let us guide you on an exciting journey to unleash the full power of APIs and modern integrations.

.png)

Embrace an architecture that is agile, scalable, and integrated

Accelerate the delivery of your digital initiatives through less complex and more efficient APIs, microservices, and Integrations that drive your business forward.